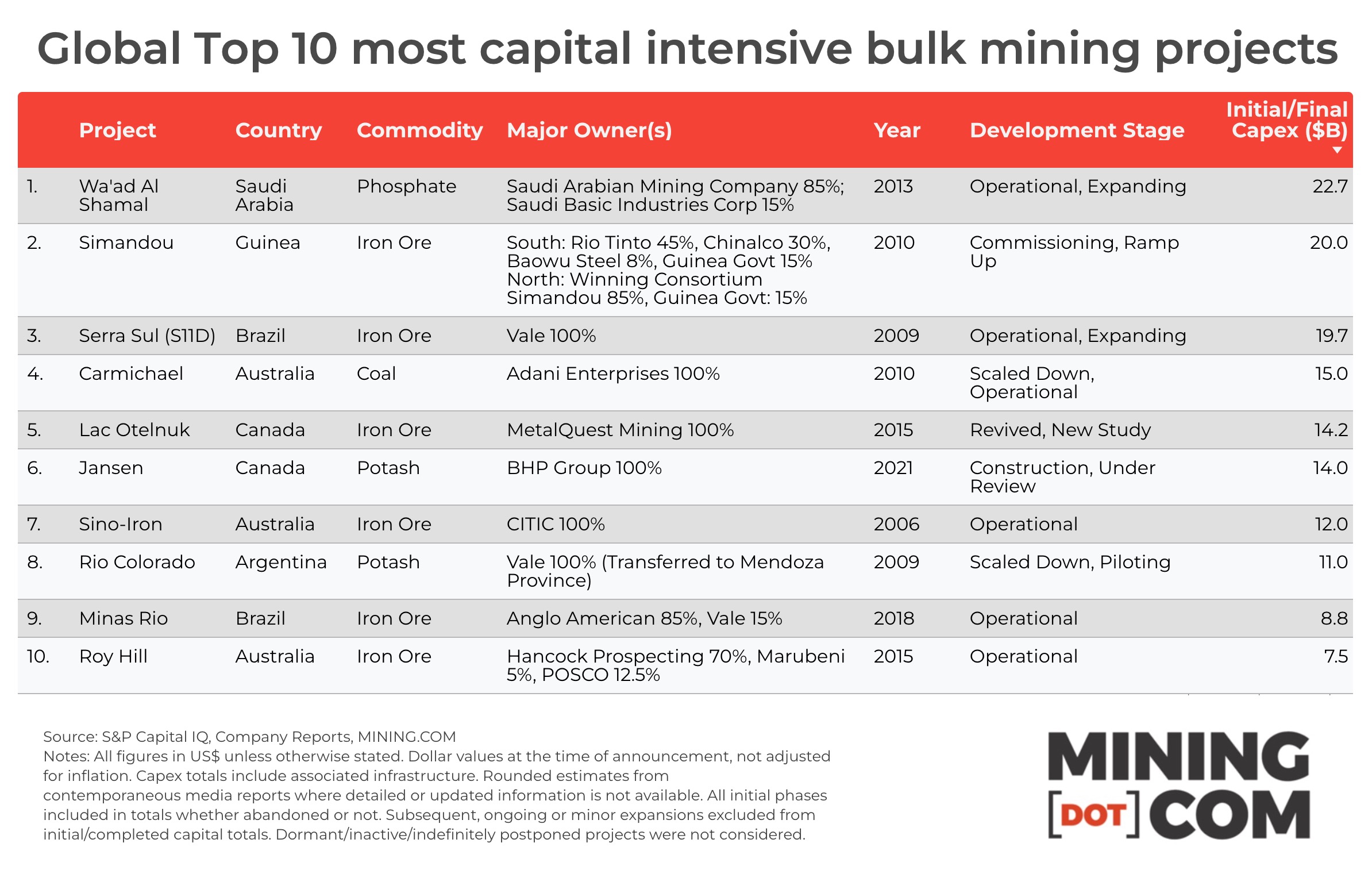

MEGAMINES: Top 10 most capital intensive bulk mining projects

Posted Under Commodity News, On 19-12-2025

Source: mining.com

With public and government attention shifting to critical minerals, energy transition metals and specialty commodities, and retail investors all-in on rampant gold and silver, here’s a reminder of where the bulk of investments in global mining and metals goes.

From 2000 to 2023, metals and mining revenues grew by $1.7 trillion, a jump of roughly 75%, affording the industry a 70% slice of the overall materials business which also includes plastics, pulp, and building materials. As a whole, materials represent some 7% of the global GDP.

However, battery and other metals associated with decarbonisation – even when lumping in bellwether copper – hardly makes up 15% of global metals and mining revenues.

Take rare earths, the commodities du jour: The market size of mining, and metal and alloy production of the 17 elements used in defence applications and green energy for wind turbines, robotics, motors for EVs and drones hover around a skimpy $20 billion.

In contrast, thermal coal and steel account for around 60%–70% of revenues. Production volumes of 7 billion tonnes and 2 billion tonnes, respectively are more than 30 times higher than all other metals and minerals combined. Output by the largest among the latter, aluminum, at roughly 100 million tonnes, does not make much of a dent in the overall total.

Bulk mining does not come cheap, and MINING.COM’s ranking* of the most capital intensive projects shows a lot can go wrong between budget allocation and steady state production.

Multi-billion dollar writeoffs are not uncommon and volatile commodities prices can shaft the best laid plans given how long these mines are in the making.

That said, when these stomach-churning capital outlays start to produce returns, they do so in spades and over generations.

1. Wa’ad Al Shamal: Saudi Arabia – Ma’aden

CAPEX (2013): $22.7 Billion

Riyadh’s Future Minerals Forum, now in its fifth year, has become an important meeting place for the capital intensive mining industry, always on the prowl for outside funding, and deep-pocketed investors.

While Saudi Arabia’s sovereign wealth fund is driving hard at diversifying its economy away from crude oil (most recently into US rare earths) and with investments beyond its borders, the Kingdom and the world’s most expensive mining project is very much a domestic undertaking.

The country’s mining champion Ma’aden completed the first stage of its Wa’ad Al Shamal phosphate complex in 2018.

While the frequently cited $22.7 billion includes state-backed total investment in the surrounding industrial city, Ma’aden’s specific capital outlay for the mining and refining components is estimated to reach $15.5 billion.

The original facility was an $8 billion investment and the ongoing Phosphate 3 expansion requires a further outlay of $7.7 billion, and is scheduled for completion by 2027.

Ma’aden recently consolidated its position by acquiring its original partner, US fertilizer producer Mosaic’s 25% stake, increasing its ownership to 85% with Saudi Basic Industries Corp holding the remainder.

Al Khabra, the primary operating mine, and the Umm Wu’al deposit in the prefeasibility stage are high-grade deposits capable of producing food and animal feed-grade products apart from fertilizer. Diammonium phosphate (DAP) export prices have been strong, topping $800 a tonne this year compared to an average of less than $600 in 2024.

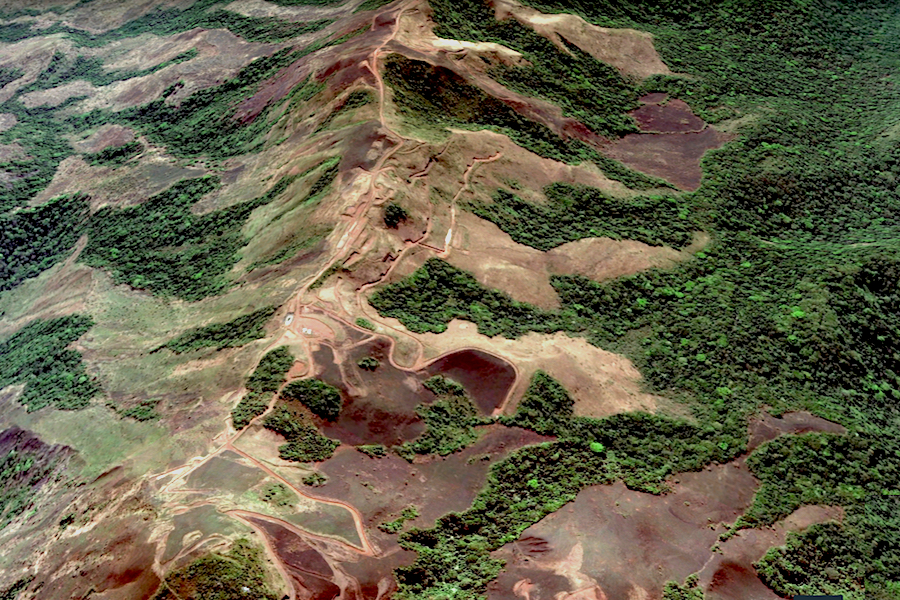

2. Simandou: Guinea – Rio Tinto, WCS

CAPEX (2010): $20 Billion+

In November after decades of stalled development, the project – a dual operation between Rio Tinto’s Simfer JV and China’s Winning Consortium Simandou – announced the official commencement of operations and the first movement of ore via the new 600km trans-Guinean railway to a new deepwater port near Guinea’s capital Conakry.

Rio Tinto was granted exploration rights as far back as 1997 and 13 years later created Simfer with Chinalco. Rio Tinto’s total funding requirement for its portion of Simandou alone is reported at approximately $11.6 billion out of overall construction costs widely projected at over $20 billion (some estimates total as much as $26 billion).

The project is divided into two primary areas: Blocks 3 & 4 owned by Simfer (Rio Tinto 45%, Chinalco 30%, Baowu Steel 8%, Guinea Govt 15%) and Blocks 1 & 2 (Winning Consortium Simandou 85%, Guinea Govt: 15%).

Simfer and WCS independently develop their mines, but the consortia jointly develop and fund the shared rail and port infrastructure (through a “true-up mechanism” to equalize costs) which is owned and operated by a separate entity, Compagnie du TransGuinéen.

With commissioning underway, the combined operation is targeting a maximum output of 120 million tonnes annually by 2028. Simandou’s strategic value lies in its premium iron ore, grading as high as 66.4% Fe.

Simandou undoubtedly will have an impact on the global market for iron ore, but whether it is a game changer and will drag down prices in a 2.3 billion tonne annual market is being debated.

Iron ore provides some of the fattest margins to producers and benchmark seaborne iron ore prices have stayed in triple digits despite bearish predictions about Chinese and world steel demand. Ore with 66% iron content sells at a premium, fetching between $120–$130 a tonne.

3. Serra Sul: Pará, Brazil – Vale

CAPEX (2009): $19.5 Billion

Vale’s Serra Sul (S11D) in Brazil ranks third with an initial $19.5 billion investment, with the bulk of the spending going on an expansion of the Carajás railroad and the Ponta da Madeira port terminal.

S11D remains the largest mining project in Vale’s history and forms part of the Rio de Janeiro-based company’s Northern System which includes mines in the Carajás complex and Serra Leste.

The project, put into production in 2017, is currently undergoing a significant brownfield expansion, the “Serra Sul +20 Mtpy” initiative, with an additional estimated investment of $2.8 billion.

This expansion, which received its operating license in September 2025 and is slated for commissioning in the second half of 2026, aims to boost the mine’s total annual capacity to 120 million tonnes.

A key differentiator is the adoption of an innovative truckless mining system, which uses mobile crushers and conveyor belts (totalling around 68 km all told including a 9.5 km single-flight) instead of traditional diesel trucks, and a dry processing system.

With total reserves of some 4.2 billion tonnes of high-grade ore, S11D is expected to be active until at least the mid-2040s or potentially as late as 2058.

4. Carmichael: Queensland, Australia – Adani Enterprises

CAPEX (2010): $15–$20 Billion

The Carmichael coal mine in Queensland, Australia, owned by Indian conglomerate Adani Enterprises is defined by its massive initial scope versus operational reality.

The initial 2010 proposal was for a massive 60 million tonnes per annum steam coal operation with a dedicated greenfield port expansion and 388 km railway line, with an estimated capital expenditure of A$16.5–A$22 billion (some $15–$20 billion in 2010 US dollar terms).

After a decade of legal, environmental and local opposition, Australian and international banks balked at providing any financing and Adani had to settle for a heavily scaled-back state one operation.

Run by Adani’s subsidiary Bravus Mining & Resources, the current mine started operations late in 2021 with a nameplate capacity of 10 million tonnes annually linked by a 200 km rail line for exports to India. A recent $500 million investment targets incremental production boosts.

Imported thermal coal prices in India are averaging around ?$130 per tonne, down roughly 30% year-over-year as domestic coal production rises and required import volumes decline.

5. Lac Otelnuk: Quebec, Canada – MetalQuest Mining

CAPEX (2015): $14.2 Billion

Lac Otelnuk, a vast iron ore deposit located in Northern Quebec on the prolific Labrador Trough, has been on hold for the better part of a decade. MetalQuest Mining (100% owner) has spent over $120 million to bring it up to the feasibility stage.

The project’s capital requirement is immense, with a 2015 study placing the cost at over $14 billion (~$19 billion in today’s money), with estimated annual output reaching a peak of 50 million tonnes per year during phase II and a mine life of 30-years.

Lac Otelnuk hosts proven and probable reserves of 4.9 billion tonnes grading 28.7% for about 1.4 billion tonnes of contained iron. The asset is geared toward producing a premium 68.5% Fe concentrate, required for hydrogen-based direct reduction, which uses hydrogen instead of coke and can significantly cut emissions in steelmaking.

The 2024 designation of high-purity iron as a critical mineral and a push by the current Canadian government to build out resources infrastructure could provide tailwinds for the project, and Metal Quest is now working on a gap analysis with AtkinsRéalis to update the 2015 study.

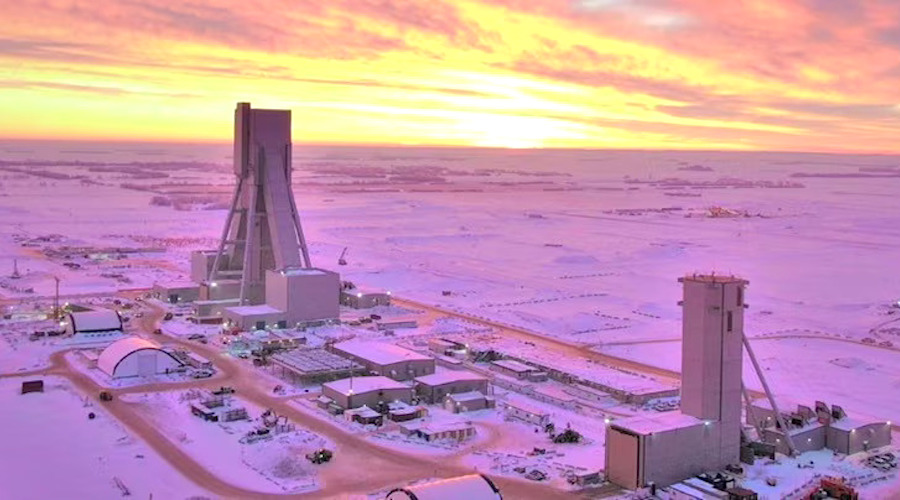

6. Jansen: Saskatchewan, Canada – BHP

CAPEX: $14 Billion

BHP’s Jansen is the single largest private economic investment in Canadian province Saskatchewan’s history with total outlays of some $14 billion if built to its full capacity.

BHP entered the Canadian potash market after a failed $40 billion takeover bid for Saskatoon-based PotashCorp (now Nutrien) in 2010, as part of efforts to diversify into “future-facing” commodities like fertilizer and copper. The company delayed sanctioning the project for over a decade due to market conditions, eventually giving the green light to the first phase in August 2021 following a multi-stage development plan.

Stage 1, initially budgeted at $5.7 billion, has been revised up to $7.4 billion due to cost overruns, with first production now anticipated in mid-2027. Stage 2 of the project was approved in October 2023 with an initial capex estimate of $4.9 billion to double the mine’s capacity to over 8 Mtpa.

However, in July this year, BHP announced it is pausing and reviewing the Stage 2 investment plan and considering a two-year delay for first production, pushing it from 2029 to 2031. The final capital cost for Stage 2 is now under review and expected to be updated in 2026.

The ultimate vision is a massive four-stage complex with 16-17 million tonnes per annum capacity, positioning BHP to become the world’s number one potash producer by leapfrogging Nutrien.

Muriate of potash at the port of Vancouver is exchanging hands for around $350 a tonne currently, up more than 20% compared to this time last year, but nowhere near the spike above $1,000 a tonne seen after the Ukraine war curtailed exports from major producers Russia and Belarus in 2022 or demand-led pricing seen early in the previous decade.

7. Sino-Iron: Western Australia – CITIC

CAPEX (2006): $12 Billion

CITIC’s Sino Iron project in Western Australia is a cautionary tale of mega-project execution, where the final cost dramatically ballooned from an initial $3 billion budget in 2006 to over $12 billion (~ $19 billion in 2025 dollars) due to engineering, design, and legal challenges.

The project is Australia’s largest magnetite mine, producing premium 65% Fe concentrate, but the low in-situ grade (~30%-35%) of the ore in comparison to Pilbara’s hematite giants added to the unhappy budget process for the Sino Iron mine.

The project’s production and expansion efforts have been significantly hampered by a protracted legal and commercial dispute with tenement holder Mineralogy Pty Ltd controlled by Clive Palmer, an outspoken billionaire politician and founder of the United Australia party.

These constraints forced CITIC to cut 2024 output by about one-third to ~14 million tonnes from previous peaks above 20 million.

A breakthrough occurred mid-year, when the legal roadblock was partially resolved, securing interim approvals that will allow CITIC to expand current operations and work toward restoring full production levels, but it will likely take years before reaching nameplate capacity of 24 million tonnes per annum.

8. Rio Colorado: Mendoza, Argentina – Vale

CAPEX (2009): $6–$11 Billion

Original capex projections for the potash project in Mendoza province, Argentina was already an eye-catching $6 billion when Vale acquired the property from Rio Tinto in 2009.

But cost overruns saw budget estimates reach as much as $11 billion. Blaming Argentina’s rampant inflation, exchange controls and a lack of government incentives, by 2013 Vale abandoned the project.

But was not before investing approximately $2.2 billion on initial mine workings and portions of the planned 800km railway and port.

The project is now owned by the provincial government of Mendoza, which transferred the assets to a new operator, Compañía Minera Aguilar in late 2023.

The current proponents are advancing a significantly scaled-down version of the project, which aims to produce 1.5 million tonnes per year, compared to the original 4.3 million tonnes per year envisaged.

The required investment for this new iteration is estimated at $1.1 billion, with a pilot plant launched in late 2024, but the lack of infrastructure to move material remains an obvious roadblock.

9. Minas Rio: Minas Gerais, Brazil – Anglo American

CAPEX (2014): $8.8 Billion

Another iron ore project with an unhappy backstory (but a happy ending) is Anglo American’s Minas-Rio complex in Brazil.

Anglo acquired the project in Minas Gerais for $5.5 billion from MMX, a company controlled by Eike Batista, Brazil’s richest man at time (later convicted of money laundering during the country’s infamous Car Wash political scandal) in a series of transactions between 2007 and 2008.

The project’s initial construction cost of $3 billion swelled to approximately $8.8 billion before production began in 2014, forcing Anglo into a $4 billion writedown of the project.

A recent $300 million investment to remove gangue is expected to add 2.8 million tonnes to current production of around 24 million tonnes of high grade ore per annum, between 2028 and 2040.

The fully integrated operation features one of the world’s longest slurry pipelines (529 km) and a dedicated port at Açu in Rio de Janeiro state

Anglo signed a partnership with Vale last year on rail and port access, avoiding building another costly slurry pipeline.

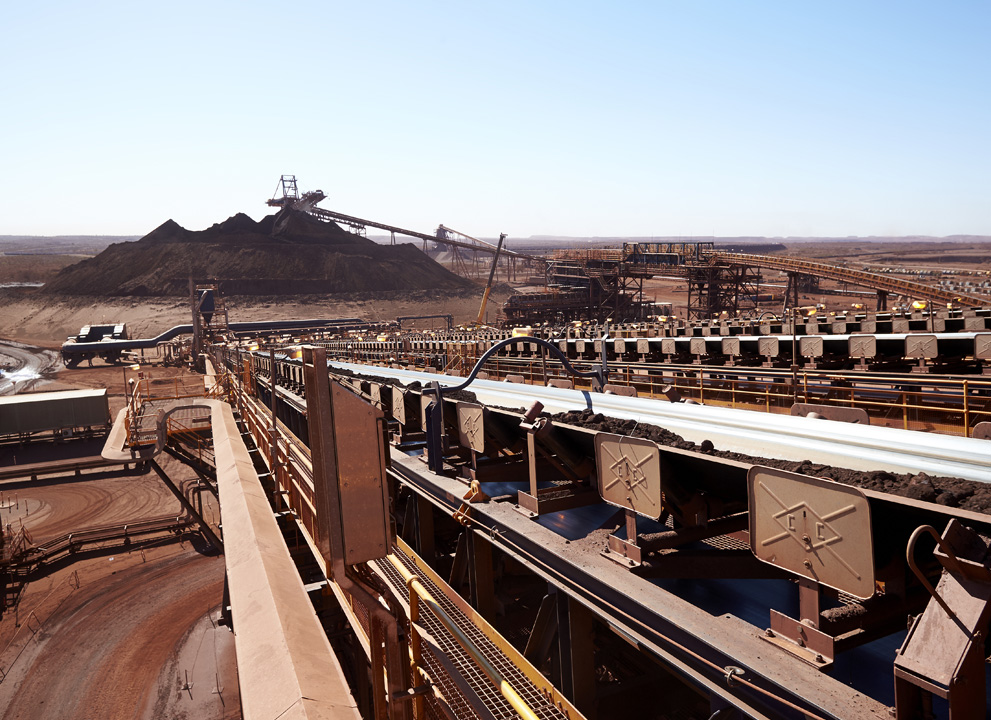

10. Roy Hill: Western Australia – Hancock Prospecting

CAPEX (2015): $7.5 Billion

Hancock Prospecting Chairman Gina Rinehart’s recent rare earth investments have paid off spectacularly, helping to boost the Australian mining doyenne’s net worth to $36 billion, up and eyewatering $20 billion just over the past year.

But Roy Hill in the Pilbara remains Hancock’s flagship asset, with the iron ore mine regularly outperforming its initial 55 million tonnes per annum design capacity since starting operations a decade ago.

Current developments to extend the life of the project beyond 2040 include the $400 million McPhee Creek satellite mine, expected to begin production in 2026. The project will feed into established infrastructure, which includes the private 344km heavy-haul railway and a dedicated port facility at Port Hedland, currently being upgraded.

The sheer size of the existing operation is underscored by the hefty A$710 million per year in annual sustaining capital.

While the development of Roy Hill was plain sailing compared to other projects in this ranking, the mine came online during a sharp correction in iron ore prices – from peaks of ?$180 per tonne in 2011 to around ?$55 per tonne by late 2015.

*Notes:

Source: S&P Capital IQ, Company Reports, MINING.COM

All figures in US$ unless otherwise stated. Dollar values at the time of announcement, not adjusted for inflation.

Capex totals include associated infrastructure. Rounded estimates from contemporaneous media reports where detailed or updated information is not available.

All initial phases included in totals whether abandoned or not.

Subsequent, ongoing or minor expansions excluded from initial/completed capital totals. Dormant/inactive/indefinitely postponed projects were not considered.